Canada

Annual Tax Planner for Canada

Organize your Canadian tax picture - employment income, RRSP deductions, provincial taxes, credits, and deductions - in a Google Sheets template you own.

In Depth

Federal, Provincial, and the Tax Planning Window

Canadian tax planning is shaped by a layered system that most other countries do not share in quite the same way. Federal and provincial taxes are calculated separately, each with their own brackets, credits, and deductions. The combined marginal rate - which can exceed 50% in several provinces at higher income levels - makes the value of every deduction worth understanding clearly.

The RRSP contribution window is one of the most consequential features of Canadian tax planning. Contributions made before the March 1 deadline reduce the previous year's taxable income, and at higher marginal rates the tax refund can be substantial. Some people use that refund to fund the current year's TFSA contribution, creating a cycle where one account effectively helps fund the other. Tracking contributions against available room throughout the year prevents last-minute scrambles or accidental over-contributions.

For self-employed Canadians, the tax picture is more complex. Both the employee and employer portions of CPP fall on you, GST/HST collection and remittance may apply, and eligible business expenses need to be tracked carefully. The June 15 filing deadline for self-employed individuals provides extra time, but any balance owing is still due April 30. Having a year-round record of income and deductions makes tax season considerably less stressful.

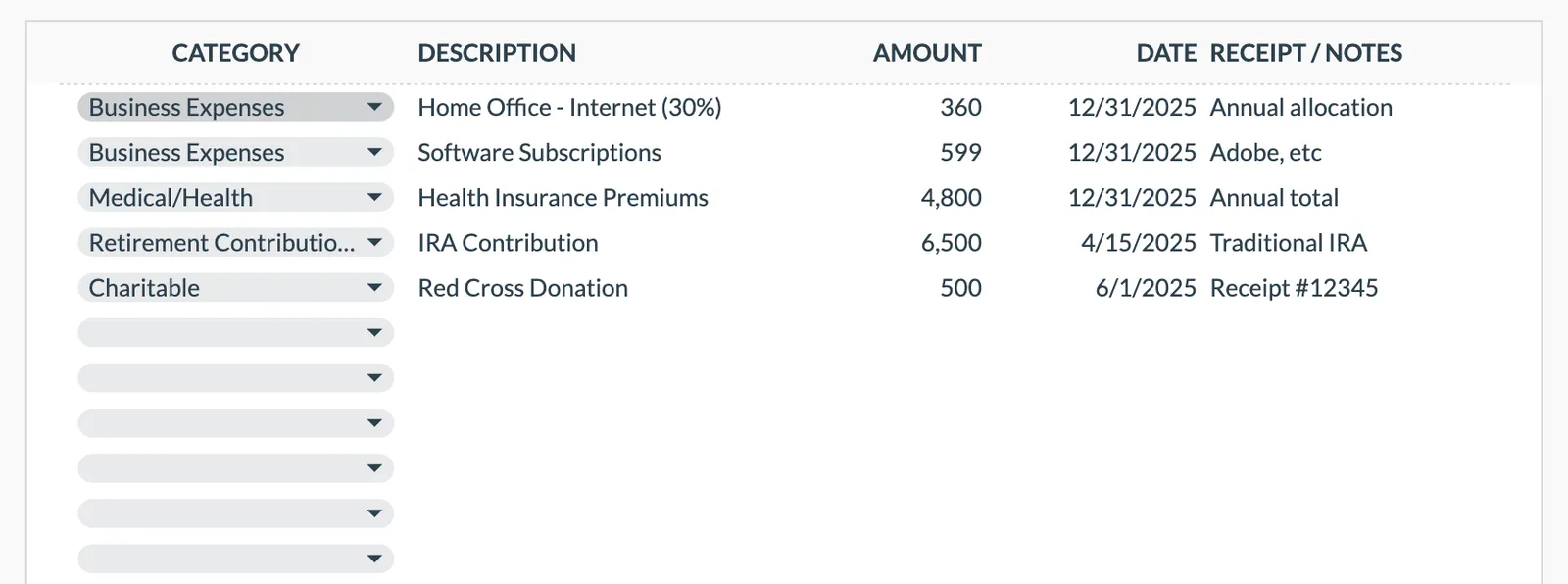

Charitable donations deserve particular attention in Canadian tax planning. The federal credit jumps from 15% to 29% (or 33% for very high incomes) on amounts above $200. Provincial credits add to this, and donation receipts can be combined between spouses to maximize the benefit. These credits are non-refundable, so they reduce tax owed rather than generating a refund on their own - but for regular donors, the savings are meaningful.

Canada

Tax Planning in Canada: Key Considerations

Canada's combined federal and provincial tax system creates opportunities for planning. Understanding the main deductions and credits helps you keep more of what you earn.

Federal and provincial taxes combine for significant rates

Federal rates range from 15% to 33%, with provincial rates stacked on top. The combined top marginal rate varies from about 44% (Nunavut) to over 54% (Nova Scotia and some other provinces). The basic personal amount ($16,129 federal for 2025) provides a tax-free base. Knowing your combined marginal rate helps evaluate the value of deductions.

RRSP contributions are the primary tax reduction tool

RRSP contributions directly reduce taxable income. At a 40% combined marginal rate, a $10,000 RRSP contribution saves $4,000 in taxes. The contribution deadline is typically 60 days after year-end (March 1 or March 2). Tracking contributions throughout the year helps maximize the deduction without over-contributing.

Canadian tax credits reduce the tax bill

Federal and provincial tax credits - medical expenses, charitable donations, tuition, disability, and climate action incentive - reduce taxes owed. The charitable donation credit is especially generous: 15% federal on the first $200 and 29-33% on amounts above $200. Tracking eligible expenses throughout the year captures all available credits.

Self-employment and rental income require careful tracking

Self-employed Canadians can deduct business expenses (home office, vehicle, supplies, professional development) against income. Rental property owners deduct mortgage interest, property tax, repairs, and other expenses. Both situations benefit from organized year-round tracking rather than scrambling at tax time.

Get the Template

Getting Started

Making the Tax Planner Work for Canadian Taxes

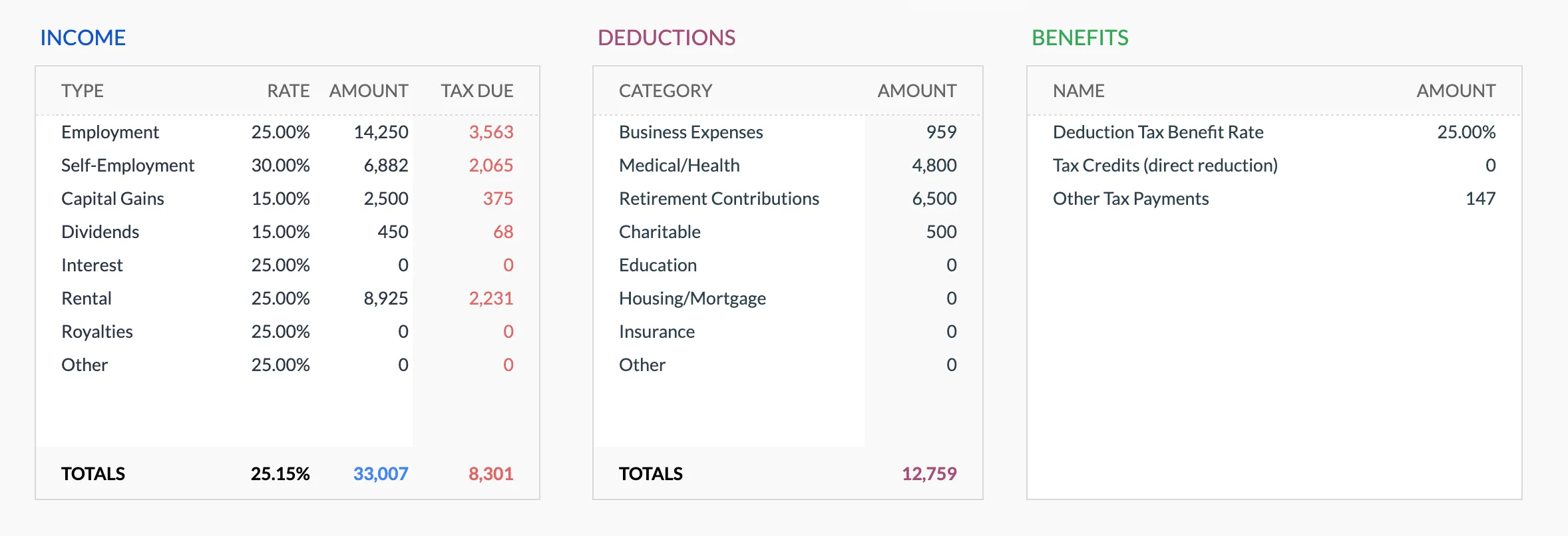

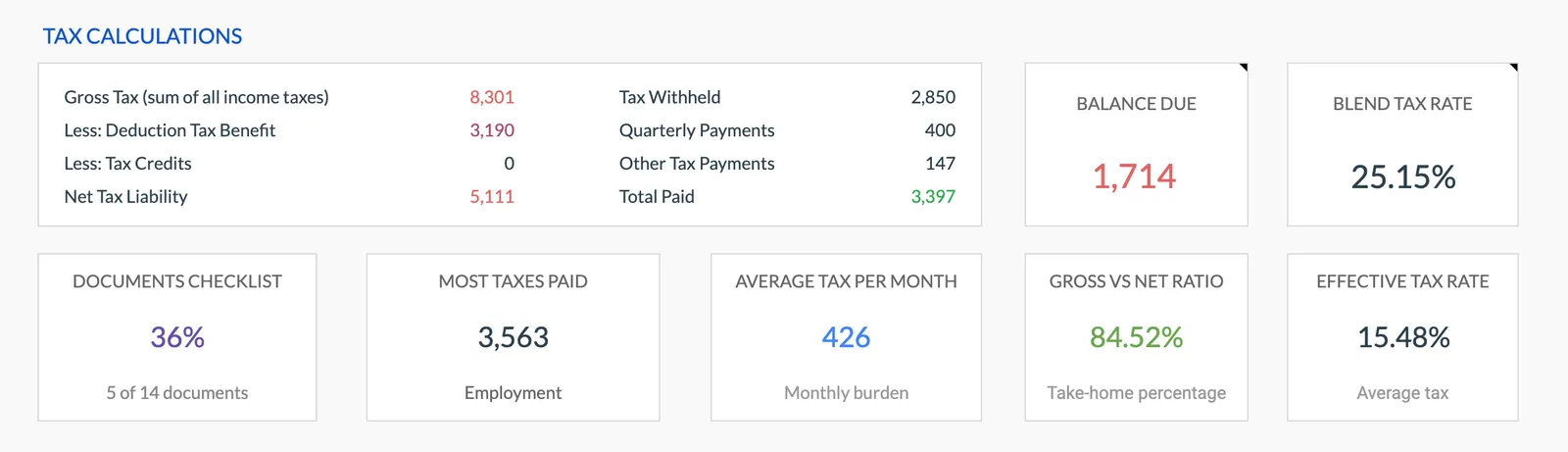

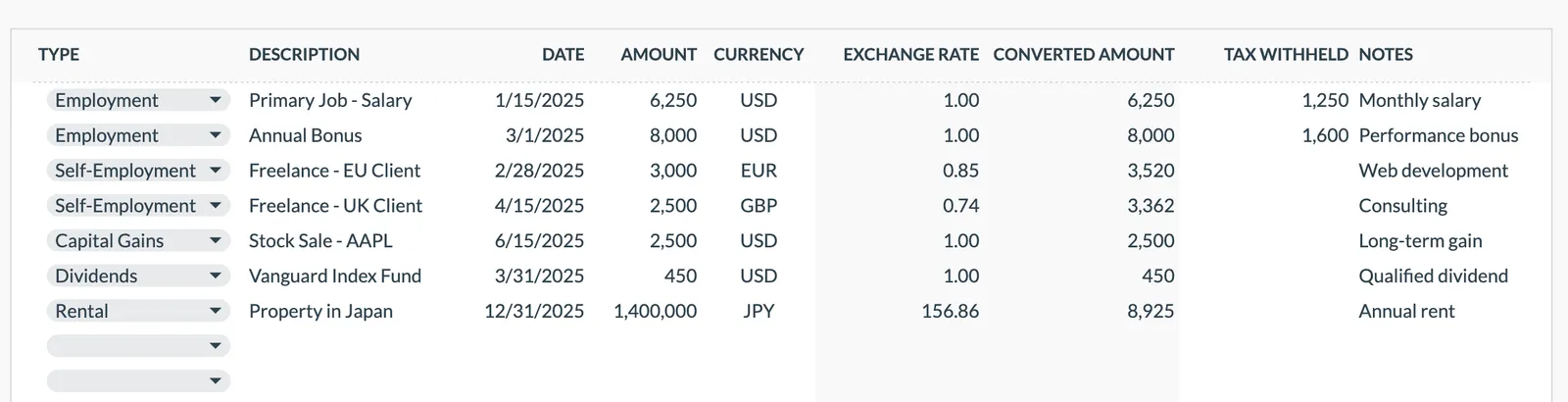

Enter all income sources

List T4 employment income, T4A contract income, T3/T5 investment income, rental income, and any other sources. Use gross figures - these are what CRA sees on your tax return.

Track deductions as they occur

Log RRSP contributions, childcare expenses, moving expenses (if you moved for work), union dues, and other deductions throughout the year. Having these ready by tax time eliminates the annual hunt for receipts.

Record eligible credit amounts

Track medical expenses (those above 3% of net income), charitable donations (keep receipts), tuition amounts, and other credit-eligible expenses. These convert to tax savings on your return.

Monitor your RRSP room

Your Notice of Assessment shows available RRSP room. Track contributions throughout the year to stay within the limit. Over-contributions beyond the $2,000 buffer are penalized at 1% per month.

Plan for tax instalments if applicable

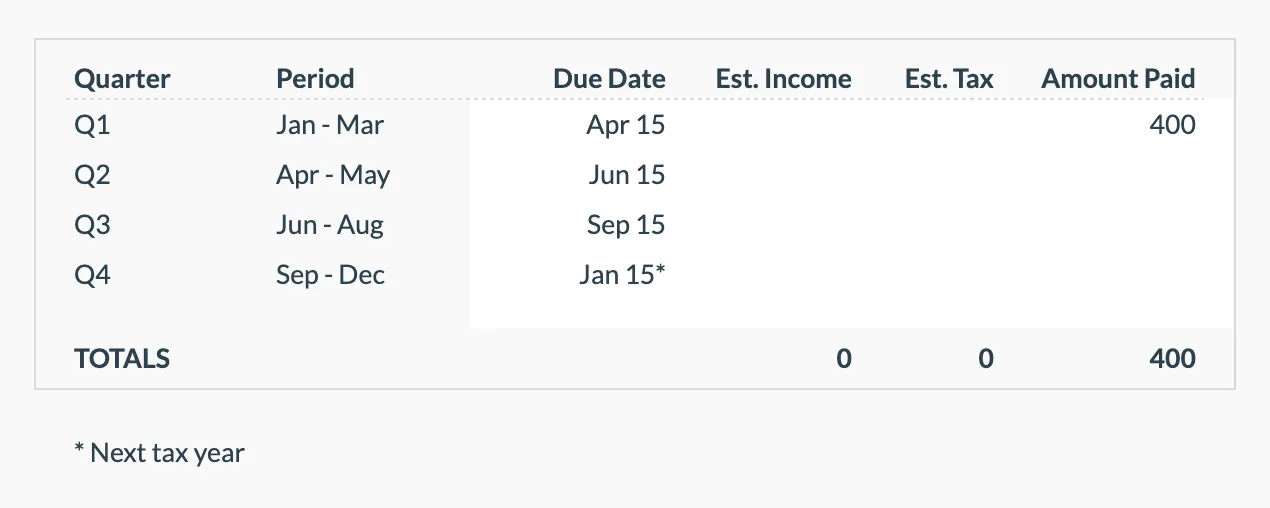

If you owe more than $3,000 in net taxes (or $1,800 in Quebec), CRA may require quarterly instalments. Track these payments to ensure they're made on time and accurately reflect your expected tax bill.

See It In Action

What the template looks like

Browse through the template to see how it handles budgeting, categories, and expense tracking - all adaptable to your local financial setup.

- Built-in currency selector

- Customizable categories

- Budget vs actual tracking

- Visual charts and summaries

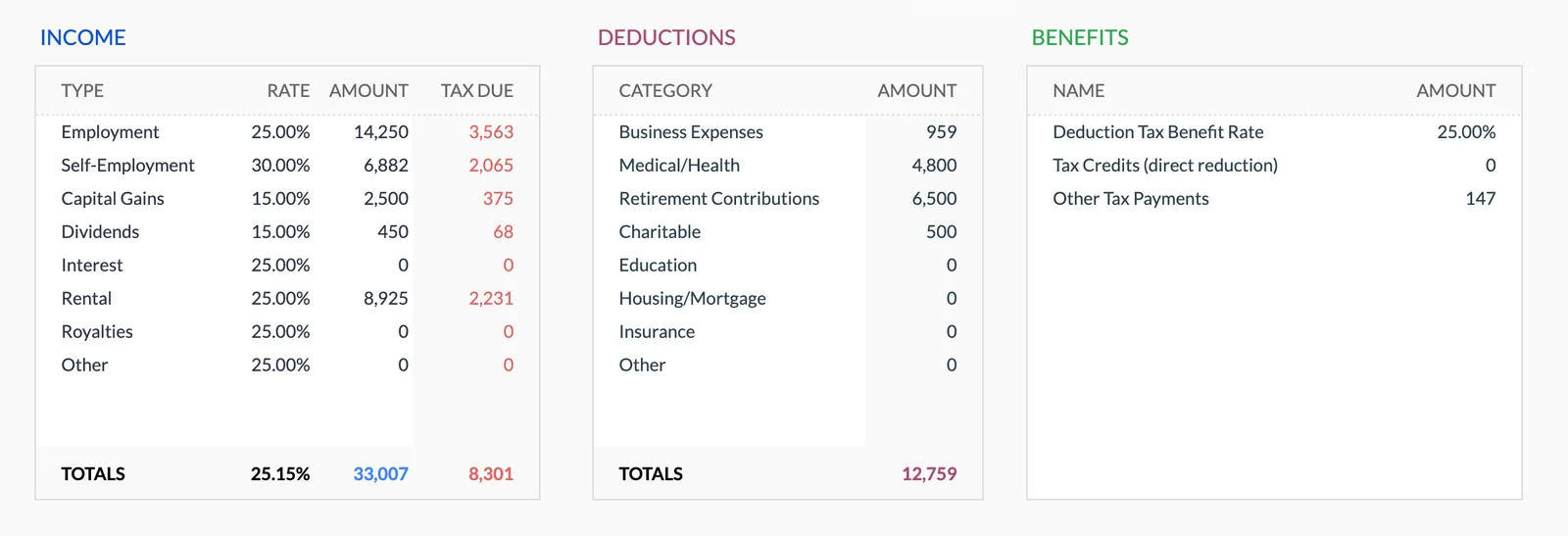

Annual tax overview with key figures

Detailed tax breakdown and projections

Track all income sources for tax purposes

Organize and track tax deductions

Plan and track quarterly estimated tax payments

Common Questions

Annual Tax Planner for Canada - FAQ

Can I file my Canadian taxes with this template?

No. This template organizes your tax-related information throughout the year. You still need to file through certified tax software (like Wealthsimple Tax, TurboTax, or StudioTax) or an accountant. The value is in having everything prepared and organized when filing time comes.

Does it calculate federal and provincial taxes?

The template organizes income and deductions but doesn't calculate the final tax bill. For estimates, use the free income tax calculator on this site or CRA's online tools.

How do I track TFSA for tax purposes?

TFSA contributions aren't tax-deductible and withdrawals aren't taxable, so they don't directly affect your tax return. However, tracking TFSA contribution room in the template prevents over-contributions, which are penalized at 1% per month.

Can I track provincial and federal separately?

Yes. You can create separate sections for federal and provincial deductions and credits. Some credits differ between federal and provincial levels. The template is flexible enough to accommodate whatever structure works for your province.

When is the Canadian tax deadline?

The general deadline is April 30. Self-employed individuals have until June 15 to file, though any balance owing is still due April 30. The RRSP contribution deadline for the prior tax year is typically March 1. The template can include these key dates as reminders.

Can't find the answer you're looking for? Contact our team

Explore More

Free Tools for Canada

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.