United Kingdom

Annual Tax Planner for United Kingdom

Organize your UK tax picture - PAYE, self-assessment income, pension tax relief, ISA usage, and capital gains - in a Google Sheets template you own.

In Depth

Making Sense of UK Tax Allowances Before April 5th

The UK tax year runs from April 6 to April 5 - a quirk dating back to calendar reform in 1752. This unusual timing means that key allowances (ISA, pension, capital gains, dividend) all reset in early April rather than January. For tax planning purposes, the months between January and April become a natural review period. Checking whether you've used your ISA allowance, whether pension contributions are on track, and whether any capital gains should be realised before the exempt amount resets can prevent wasted allowances.

The interaction between income tax bands and pension contributions is one of the most valuable planning opportunities in the UK system. Higher-rate taxpayers (40%) who contribute to a pension effectively get their money boosted by the tax they would have paid. For someone earning £60,000, a £10,000 pension contribution costs only £6,000 in real terms after tax relief. At incomes between £100,000 and £125,140, the effective marginal rate hits 60% due to the personal allowance taper - making pension contributions in this range exceptionally tax-efficient.

Self-assessment affects a growing number of UK taxpayers beyond the self-employed. Anyone with income above £150,000, rental income, foreign income, or certain investment income exceeding specific thresholds may need to file. Payments on account - advance tax payments due on January 31 and July 31 - catch some people off guard in their first year of self-assessment. A tax planner that tracks income sources throughout the year and flags upcoming payment deadlines reduces the January rush and the risk of penalties for late filing.

United Kingdom

Tax Planning in the United Kingdom: Key Considerations

The UK tax system combines PAYE withholding with self-assessment for some taxpayers. Understanding the main allowances and rates helps you plan effectively.

Income tax bands and the personal allowance

The personal allowance (£12,570 for 2025-26) means no tax on the first £12,570 of income. The basic rate is 20% (up to £50,270), higher rate 40% (up to £125,140), and additional rate 45% above that. The personal allowance tapers for income above £100,000 - effectively creating a 60% marginal rate between £100,000 and £125,140.

Self-assessment adds complexity for some

If you have self-employment income, rental income, investment income over £10,000, or income over £150,000, you'll likely need to file a self-assessment tax return. Tracking these income sources throughout the year makes the January 31st filing deadline less stressful. Payments on account (advance tax payments) are required if your tax bill exceeds £1,000.

Pension contributions offer significant tax relief

Pension contributions receive tax relief at your marginal rate. For higher-rate taxpayers, contributing to a pension effectively costs 60p for every £1 invested (when accounting for employer NI savings in salary sacrifice). The annual allowance is £60,000 (2025-26) with unused allowance carried forward up to three years.

Capital gains have their own rules

The capital gains annual exempt amount is £3,000 (2025-26), down significantly from previous years. Capital gains above this are taxed at 18% (basic rate) or 24% (higher rate) for most assets. ISA and pension investments are exempt from capital gains tax, making the annual ISA allowance even more valuable.

Get the Template

Getting Started

Making the Tax Planner Work for UK Tax Rules

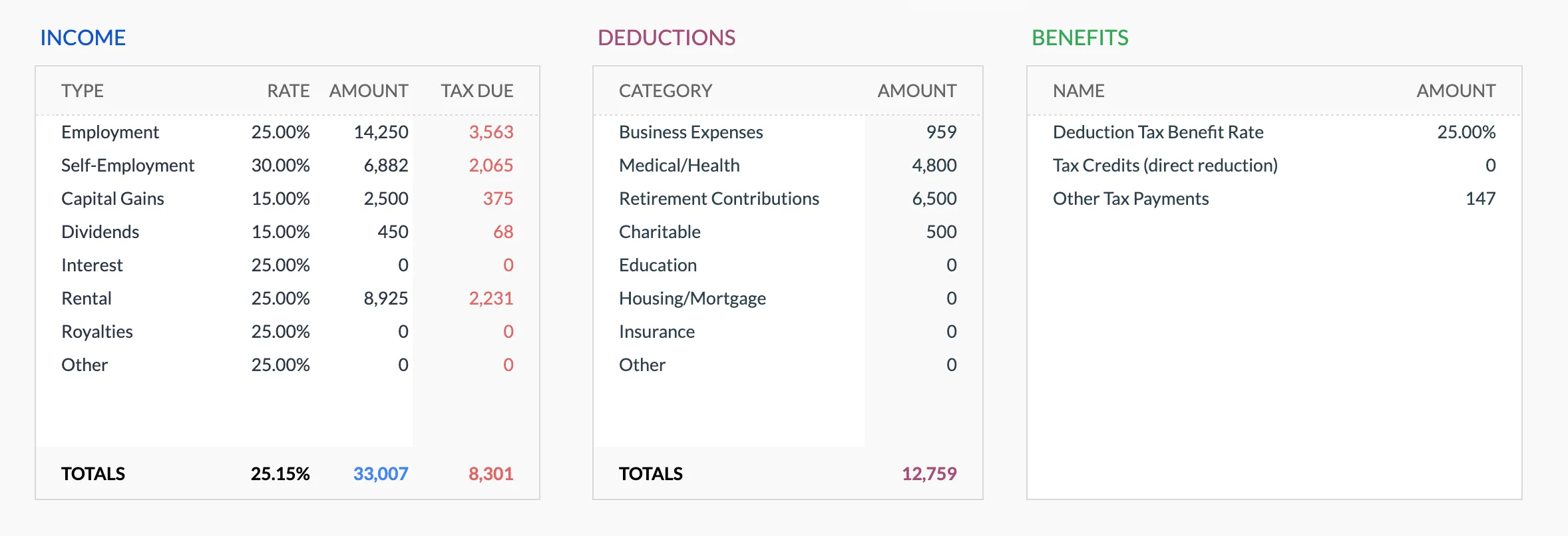

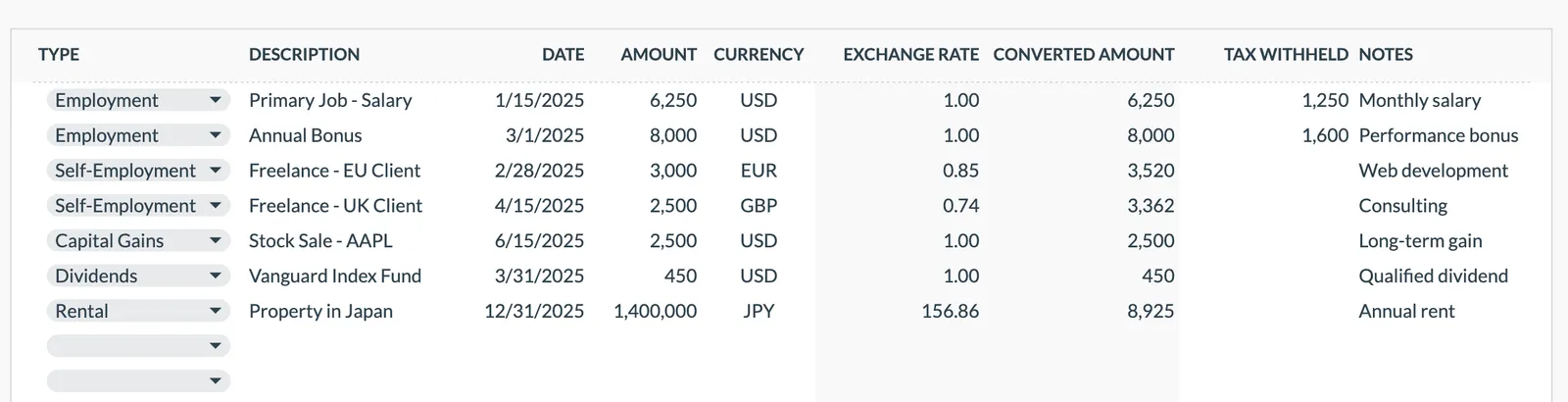

Enter all income sources

List employment income (gross, from your P60 or payslips), self-employment profits, rental income, dividend income, savings interest, and any other sources. Gross figures are needed for tax planning even though you receive net pay.

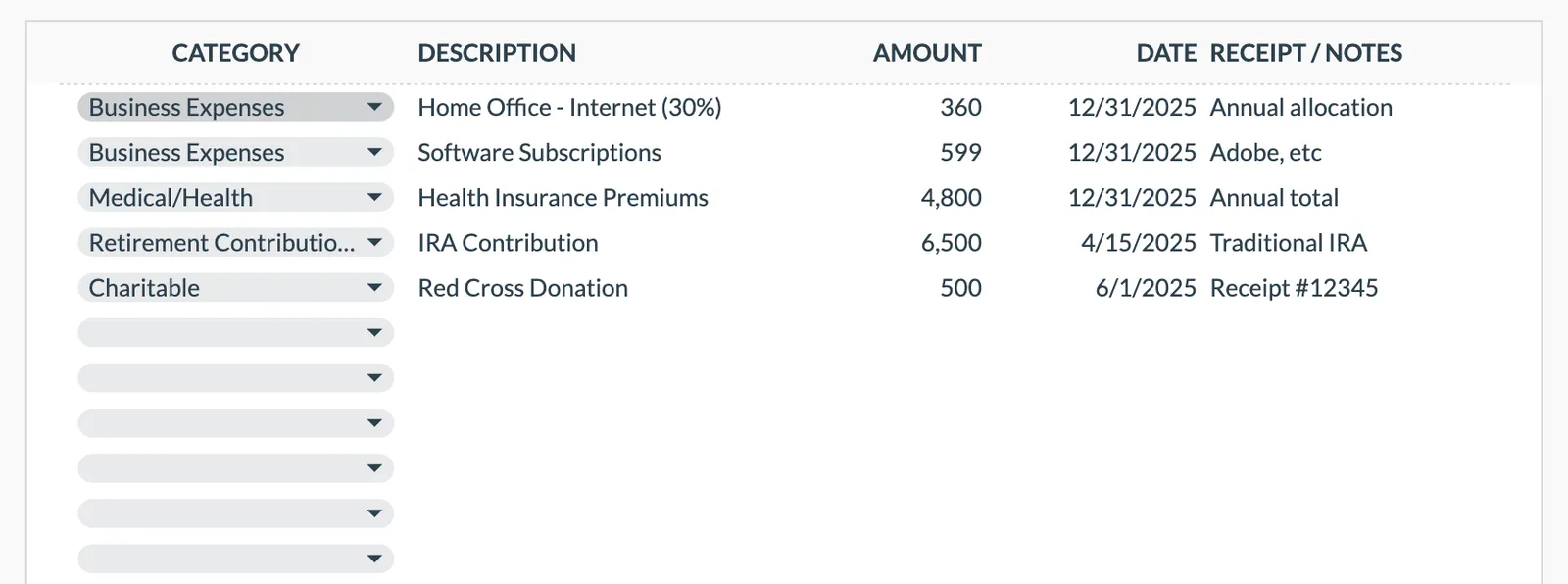

Track tax-deductible expenses and reliefs

Log pension contributions (for additional tax relief claims), Gift Aid donations (which extend your basic rate band), allowable business expenses for self-employment, and any other tax-deductible items.

Monitor allowance usage

Track your ISA allowance (£20,000), pension annual allowance (£60,000), personal savings allowance (£1,000 basic rate, £500 higher rate), dividend allowance (£500), and capital gains exempt amount (£3,000). The template can show progress against each.

Plan pension contributions strategically

For higher-rate taxpayers, pension contributions are especially tax-efficient. Track contributions made by your employer (via salary sacrifice) and any personal contributions to stay within the annual allowance while maximizing tax relief.

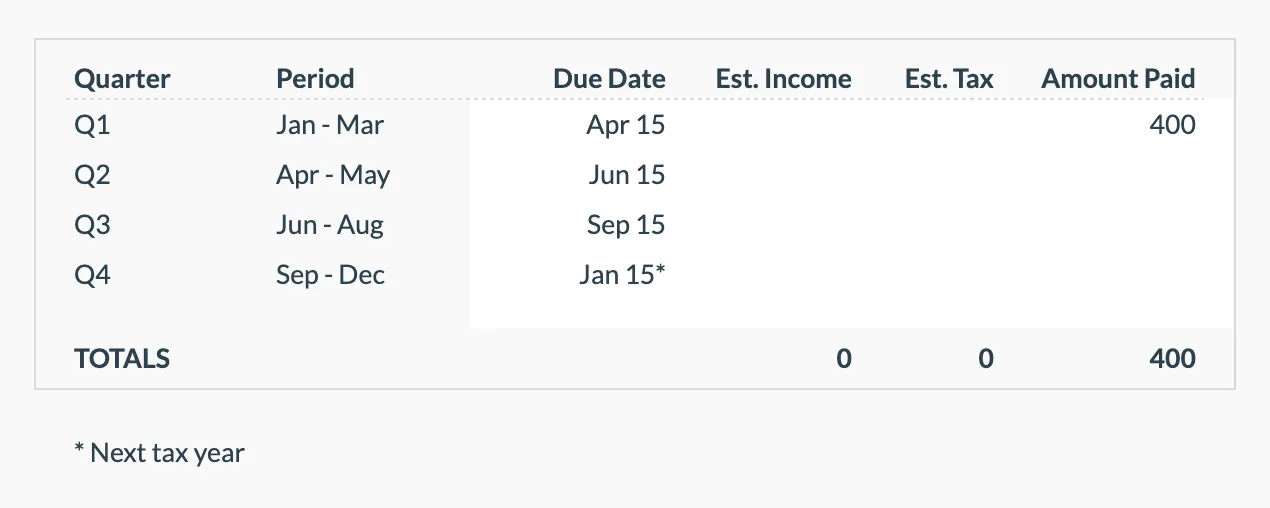

Prepare for self-assessment deadlines

If you file self-assessment, track payments on account (due January 31 and July 31) and the balancing payment. Having income and expense figures organized throughout the year makes filing faster and reduces the risk of errors.

See It In Action

What the template looks like

Browse through the template to see how it handles budgeting, categories, and expense tracking - all adaptable to your local financial setup.

- Built-in currency selector

- Customizable categories

- Budget vs actual tracking

- Visual charts and summaries

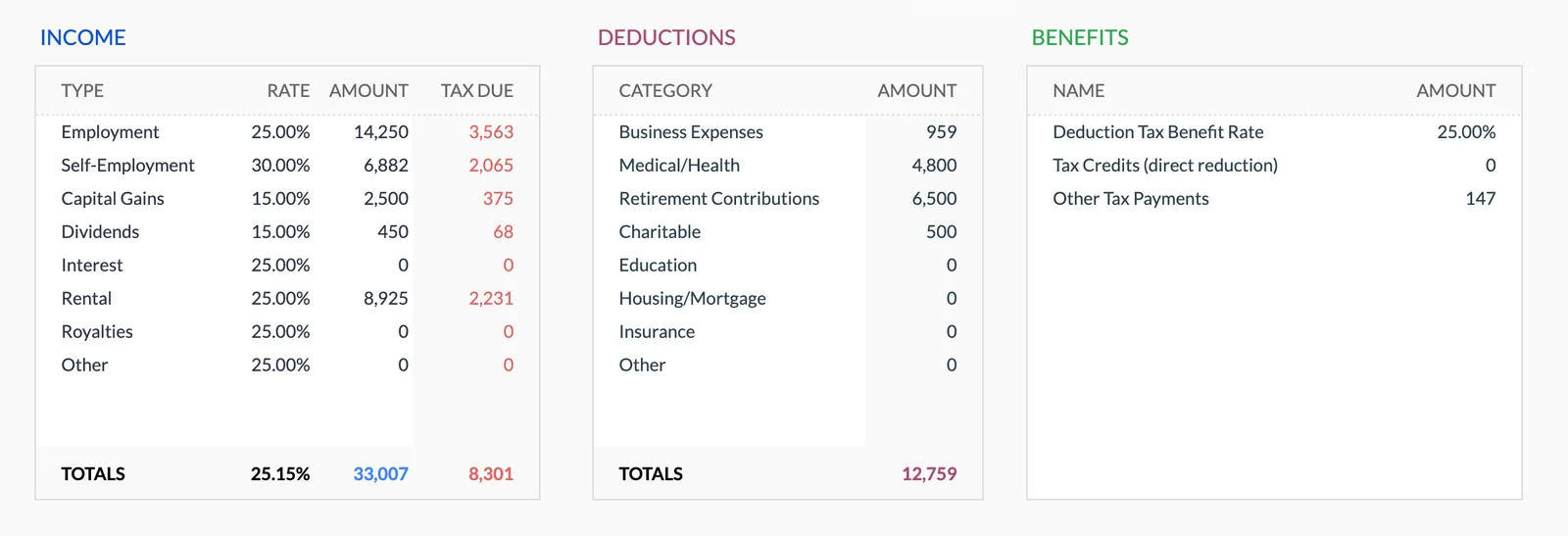

Annual tax overview with key figures

Detailed tax breakdown and projections

Track all income sources for tax purposes

Organize and track tax deductions

Plan and track quarterly estimated tax payments

Common Questions

Annual Tax Planner for United Kingdom - FAQ

Does this replace self-assessment filing with HMRC?

No. This is a planning template that helps organize your tax-related information throughout the year. You still need to file through HMRC's online self-assessment portal or use an accountant. The template makes that process easier by keeping everything in one place.

Does it calculate my tax bill?

The template organizes your income and deductions but doesn't calculate the final tax amount. For estimates, use the free income tax calculator on this site or HMRC's own tax checker tools.

How do I track pension tax relief?

If your employer uses salary sacrifice, the tax relief is automatic. For personal pension contributions (SIPP), the provider claims basic rate relief (20%) automatically - you need to claim higher/additional rate relief through self-assessment. Track both types to see total relief received.

Can I track my partner's tax situation too?

UK taxes are individual, not joint (unlike the US). You can add a second set of entries for your partner, which is useful for planning things like marriage allowance transfers or splitting capital gains across both CGT allowances.

When does the UK tax year start?

The UK tax year runs from April 6 to April 5. This is different from the calendar year and catches many people off guard. ISA, pension, and CGT allowances all reset on April 6, so March is often a good time to review whether you've used your annual allowances.

Can't find the answer you're looking for? Contact our team

Explore More

Free Tools for United Kingdom

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.