United Kingdom

FIRE Calculator for United Kingdom

Calculate your path to financial independence - factoring in ISAs, SIPPs, State Pension, and UK-specific tax rules - in a free Google Sheets calculator.

In Depth

Why the UK Is Quietly One of the Better Places for FIRE

The UK offers several structural advantages for financial independence that aren't always obvious at first glance. The NHS means healthcare costs in early retirement are effectively zero for most people - a stark contrast to the US, where healthcare is often the single largest FIRE planning variable. ISAs provide £20,000 per year of completely tax-free saving and investing with no restrictions on withdrawals. And the State Pension, while not enough to live on alone, acts as a guaranteed income floor that reduces how much your portfolio needs to sustain in later years.

The typical UK FIRE strategy uses a two-phase approach. Before pension access age (currently 55, rising to 57 in 2028), spending comes from ISAs and general investment accounts - both accessible without penalties at any age. After pension access age, SIPP withdrawals kick in, with 25% available tax-free. This bridge period is the key planning challenge, and it's why maximizing ISA contributions each year is central to most UK FIRE plans. A decade of maxing out a Stocks and Shares ISA can build a substantial tax-free bridge fund.

Cost of living plays a huge role in UK FIRE numbers. Someone targeting financial independence in London faces a fundamentally different calculation than someone in Wales, northern England, or Scotland. Housing costs alone can differ by a factor of three or more. Many UK FIRE practitioners factor in geographic flexibility - the possibility of moving to a lower-cost area - as a lever that can reduce their target number significantly. A FIRE calculator that lets you model different spending levels makes this comparison concrete rather than speculative.

United Kingdom

FIRE in the United Kingdom: What to Know

The FIRE movement has a growing UK community, with some advantages over other countries - notably the NHS, ISA allowances, and generous pension tax relief.

The NHS removes healthcare from the equation

Unlike the US, where healthcare costs are a major FIRE challenge, the NHS provides free-at-point-of-use healthcare regardless of employment status. This significantly reduces the annual spending figure that drives your FIRE number. Private health insurance is optional, not essential.

ISAs and SIPPs provide a powerful tax-efficient combination

ISAs (£20,000/year, completely tax-free withdrawals) are ideal for pre-pension-age spending in early retirement. SIPPs provide tax relief on contributions and tax-free growth but are locked until age 55 (57 from 2028). A typical UK FIRE strategy fills ISAs for the bridge period and SIPPs for later retirement.

The State Pension reduces the required portfolio size

The full State Pension (£11,500+/year) kicks in at State Pension age and reduces how much your investment portfolio needs to provide. This means the FIRE number for UK residents can be lower than the simple 25x calculation suggests, once you account for this future income stream.

UK FIRE numbers tend to be lower than US equivalents

Between the NHS, State Pension, and generally lower cost of living outside London, many UK FIRE practitioners find their target numbers are lower than American equivalents. A couple targeting a moderate lifestyle outside London might aim for £500,000-800,000 in invested assets, plus eventual State Pension.

Get the Template

Getting Started

Running Your UK FIRE Numbers With ISAs and Pensions

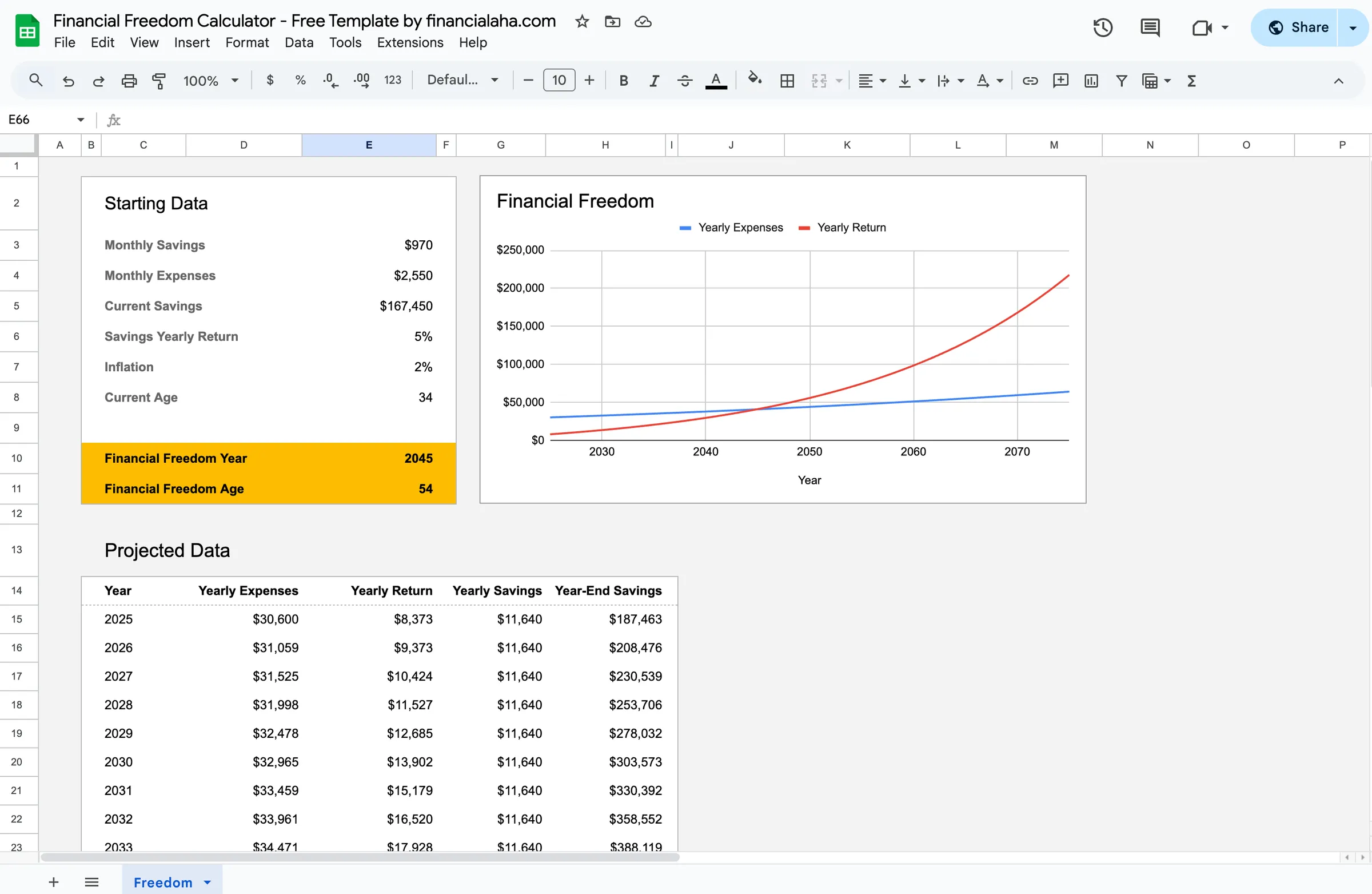

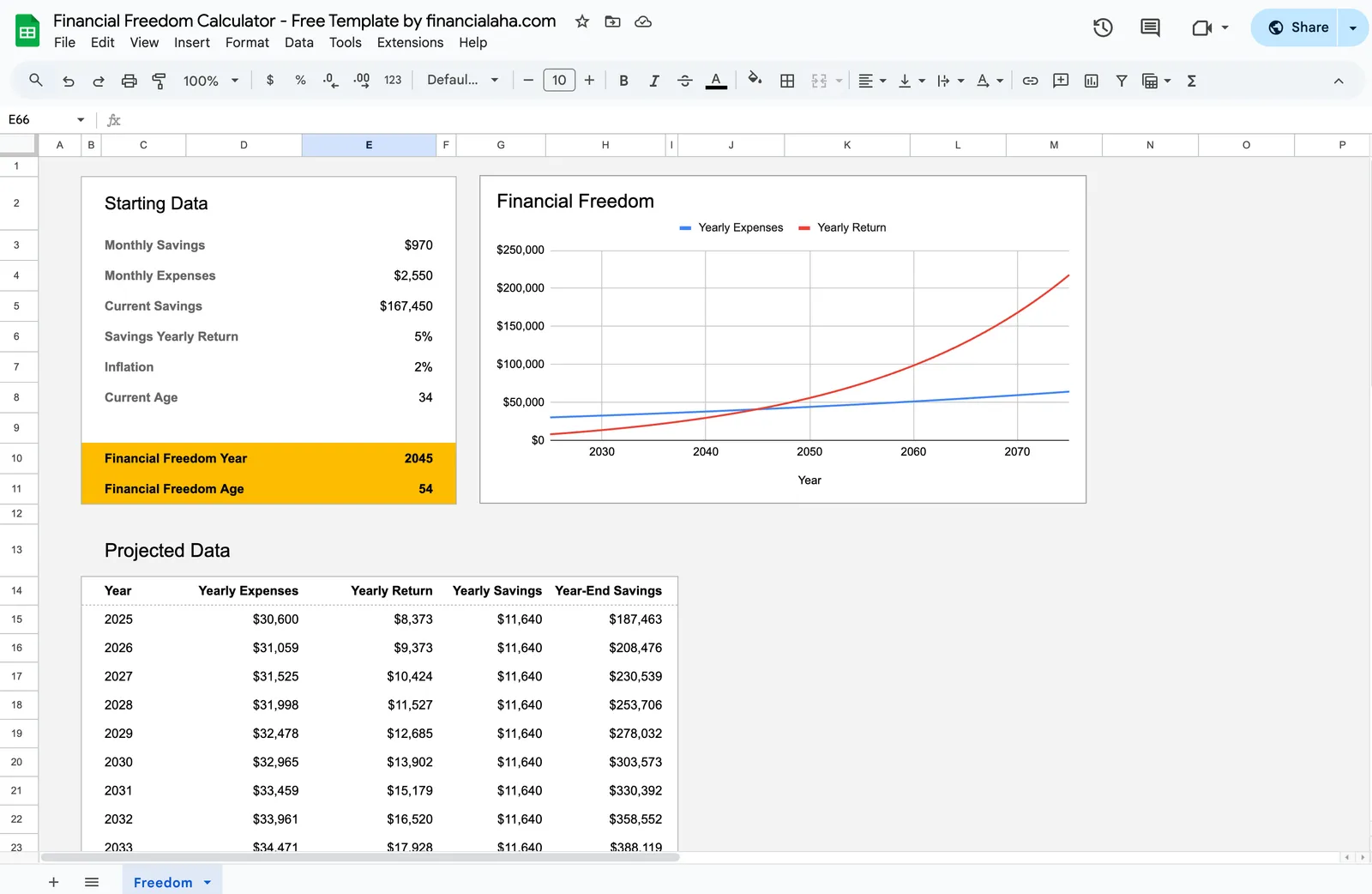

Enter your current invested assets

Input total values across ISAs (Cash and Stocks & Shares), SIPPs, workplace pensions, GIAs, and any other investments. Include everything you're counting toward financial independence.

Set your target annual spending

Enter your expected annual expenses in early retirement. Since the NHS covers healthcare, this mainly includes housing, food, utilities, transport, leisure, and insurance. Be realistic - look at your actual spending as a guide.

Add your annual savings amount

Enter how much you invest each year. Include ISA contributions, pension contributions (including employer match and tax relief), and any GIA investments. Your savings rate is the primary driver of your FIRE timeline.

Factor in future State Pension income

Enter your projected State Pension amount and the age you'll receive it. This reduces the long-term portfolio requirement since the State Pension provides a baseline income you don't need to fund from investments.

Review your projected FIRE date

The calculator shows when your investments can sustain your target spending. Experiment with different savings rates and spending levels to see how sensitive the date is to changes.

See It In Action

What the template looks like

Browse through the template to see how it handles budgeting, categories, and expense tracking - all adaptable to your local financial setup.

- Built-in currency selector

- Customizable categories

- Budget vs actual tracking

- Visual charts and summaries

Calculate your path to financial independence

Common Questions

FIRE Calculator for United Kingdom - FAQ

Is this FIRE calculator really free?

Yes. The FIRE calculator is completely free - no payment, no email required. It runs in Google Sheets so you own and control your data.

How do I access pension money before 55?

You can't access a SIPP or workplace pension before 55 (57 from 2028) without extreme circumstances. The UK FIRE strategy typically uses ISAs and GIA investments for the bridge period between early retirement and pension access age. This is why ISA contributions are so important for UK FIRE planning.

What is a typical UK FIRE number?

It depends entirely on annual spending and whether you account for the State Pension. Someone spending £30,000/year might target £750,000 (25x). With future State Pension of £11,500/year, the portfolio only needs to cover £18,500/year once you reach State Pension age - which means the long-term target could be lower.

Does the 4% rule work in the UK?

The 4% rule was based on US market data, but similar analyses of global markets suggest 3.5-4% is a reasonable range. Some UK FIRE planners use 3.5% for added safety, especially for very long retirements (40+ years). The State Pension also provides a floor that reduces reliance on the portfolio alone.

How important is the ISA allowance for FIRE?

Very important. The £20,000 annual ISA allowance provides tax-free growth and withdrawals - no capital gains tax, no income tax on interest or dividends. For FIRE, ISAs are the primary vehicle for the pre-pension bridge period. Maximizing ISA contributions each year is a cornerstone of most UK FIRE strategies.

Can't find the answer you're looking for? Contact our team

Explore More

Free Tools for United Kingdom

Ready to get started?

Download instantly and start managing your finances, or contact us to design a custom template package for your needs.